Data Centres & Energy

An update on demand-pull for the clean energy technologies

We have been somewhat reticent - too reticent really - to expound much on this topic since there is so much ink being spilt across our industry press, a lot of hot takes, quite a bit of hyperbole. But, whilst it is true that data centre power demand is nowhere near the top of the list for energy demand growth globally, it is BY FAR the most important source of marginal power demand in the US (our main market). This is both in terms of absolute numbers and, as important, the urgency of the organisations driving it. The big tech companies, the deepest-pocketed companies that have ever existed, deem it an existential imperative to scale compute resources as fast as possible. I wrote about this first two years ago, when the shift to a regime of demand growth was just starting to kick in. At the time, there were early signs of pull-forward of certain technologies (mostly nuclear) to fill this demand. Since then, the hyperscalers and the big data centre developers have proved to be the most important end customer for multiple technologies moving into commercialisation. This is an update on these dynamics and an opportunity to briefly share the different areas of technology pull-through we’re seeing. It is not supposed to be comprehensive and doesn’t cover the AI application layer as it applies to the energy system, which is also a rich opportunity area.

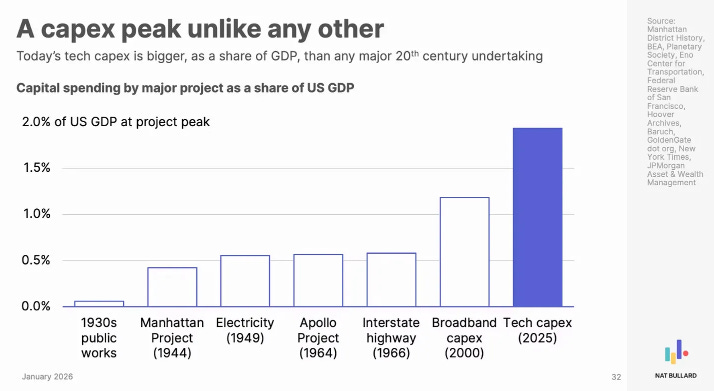

Just to set a little context on the scale of this buildout, the capital spending from a small number of tech companies, the hyperscalers - Meta, Google, Microsoft, Amazon - plus OpenAI and Anthropic, represents a higher % of GDP than any of the major infrastructure or government sponsored technology programmes over the last century. Recycling here a chart from Nat Bullard included in my January post:

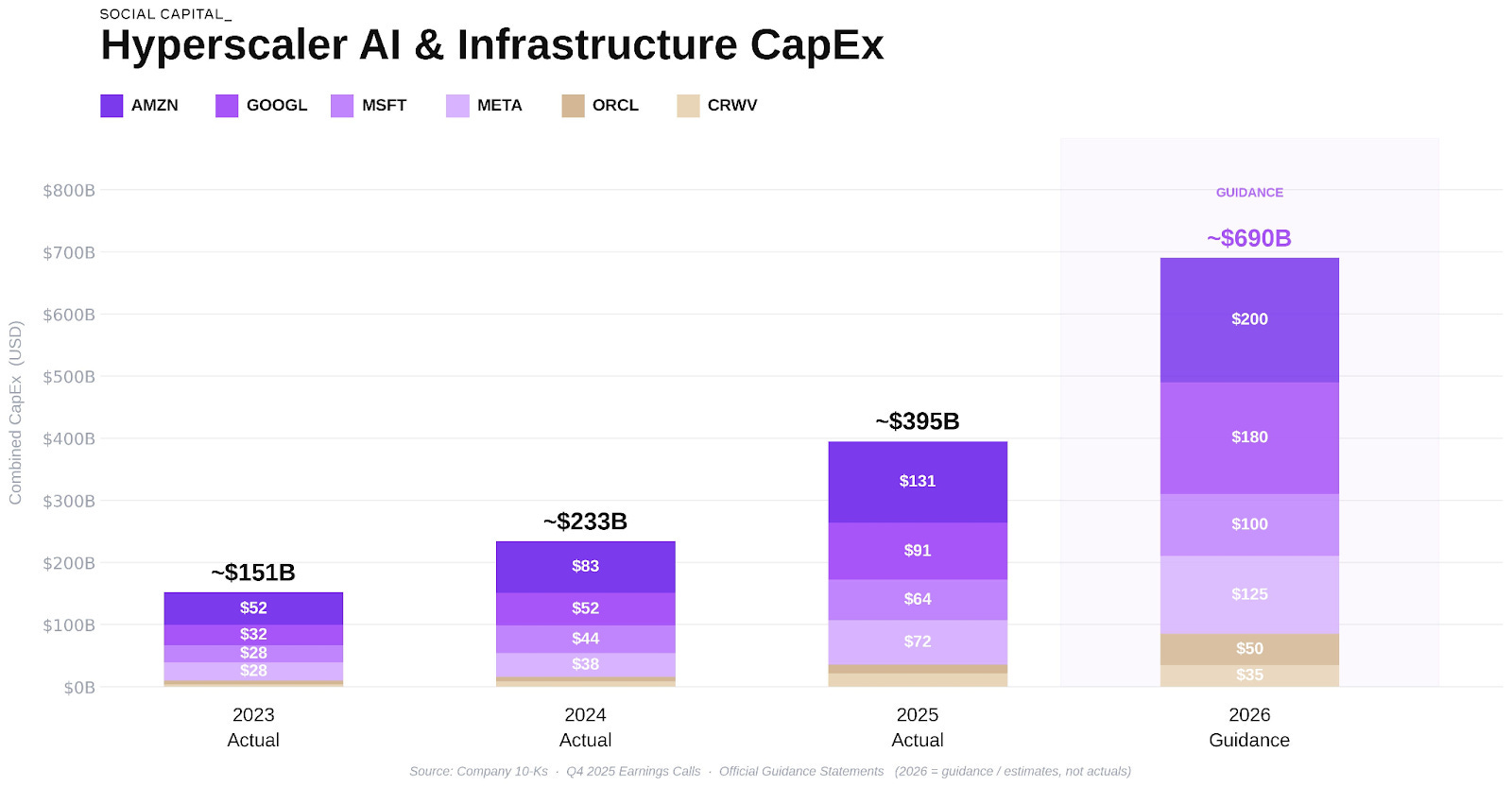

To put that into dollars and cents, that is $600bn this year alone amongst the four hyperscalers, and almost $700bn when you add in Oracle and Coreweave.

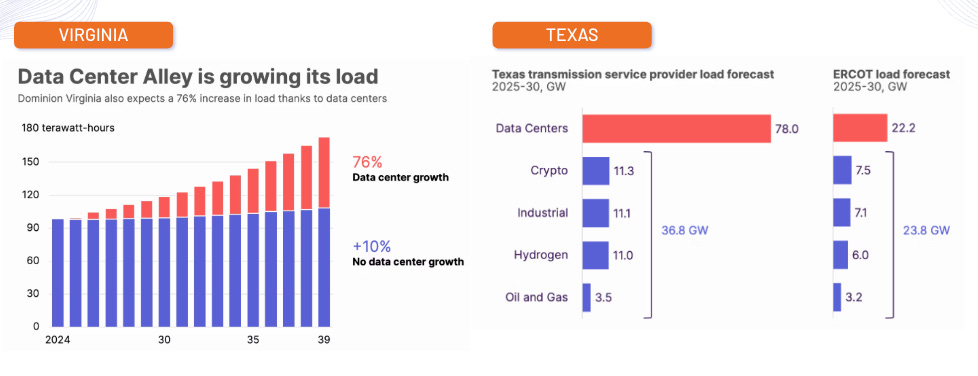

As mentioned, whilst data centre power demand growth is nowhere close to the top of global drivers of electricity demand (that is industry, by a margin, with cooling also coming in ahead of data centres), they are absolutely the most important driver in the US as a whole and particularly in certain grids.

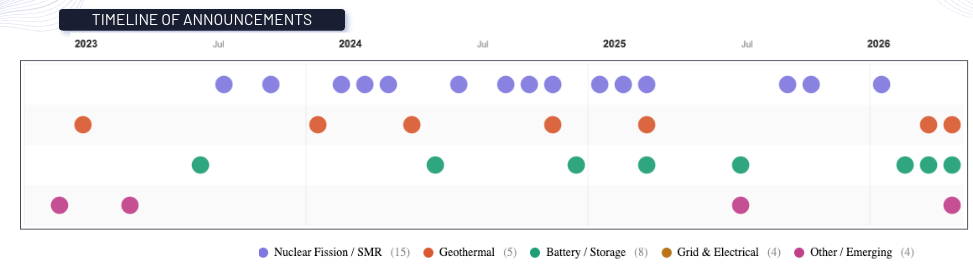

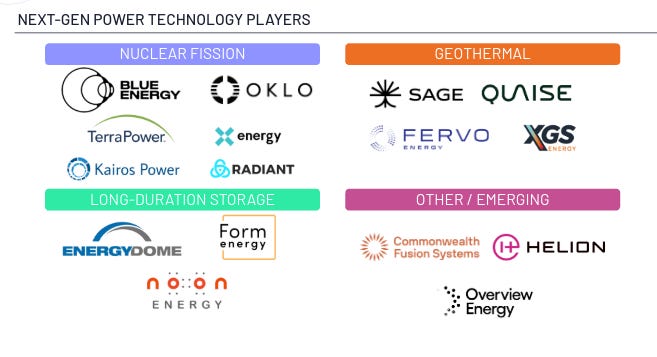

Importantly this demand growth represents a paradigm shift in load growth, compared to, say, China, where nobody really talks about data centres because they’ve been used to 4-6% annual demand growth for 30 years. The gear shift to growth, combined with extreme urgency and deep pockets of the key customers has resulted in a sharp pull-forward of generation technologies. We shared this slide in our Q1 investor update six weeks ago, and even since then I’ve had to update with several data points:

All of these announcements represent flagship early projects for the power companies. The highest number of partnerships are on the nuclear fission side, all still several years out from delivering power. Geothermal is a bit more proximate, with Fervo already having done a pilot project with Google and publicly announced a 3GW framework agreement with Google alongside their S-1 for their imminent IPO. On the energy storage side, the most proximate deployment seems to be Form Energy’s project with Google, which will start to come online in phases from 2028. Moving more to the frontier, Microsoft and Google have offtakes with nuclear fusion companies (Helion and CFS respectively) and Meta just announced a deal with Overview Energy to beam energy down from space to be converted by terrestrial solar farms. And this doesn’t even begin to get into Elon’s data centres in space, remote wave-powered data centres, or, more near term, edge data centres at the home.

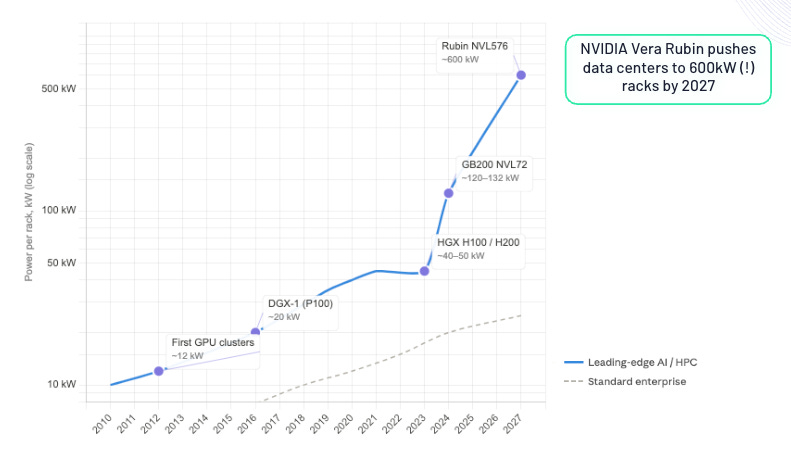

Access to power and speed to power is where we’ve seen a lot of headline grabbing partnerships. But another dynamic driving the demand pull-through for clean energy technologies is the increasing energy density, as the power ratings of bleeding-edge GPUs has been rising exponentially.

As the racks themselves have moved from 15-30kw to 150kw and soon to more than 500kw, that massively increases complexity and requires new generation of technologies from cooling (e.g. XNRGY) to transformers (Heron Power) to optics (Mojo Vision) and high-temperature superconductors to allow high-voltage DC power within the data centre (VEIR). The requirement for “four 9’s” (99.99%) or “five 9s” (99.999%) of reliability is also increasingly being recognised as a constraint to the pace of bringing on new compute and requiring massive overbuild. A report from Duke University suggested that avoiding 1% of peak hours would reduce demand for natural gas combined cycle turbines by 10-15%. Companies like Emerald AI are stepping in to provide the orchestration that allows that flexibility to be realised, even as the hyperscalers are starting to think about relaxing the reliability criteria to accelerate the overall amount of compute they can bring online.

We often hear it being pointed out that this particular infrastructure boom is unlike previous cycles as so much of the spend is going into chips (roughly ⅔ of the cost of the data centre), not railroad steel or interstate highways or even fibre optic cables that have decades of use. However, looking at demand pull from the major tech companies, the sense of urgency, the depth of capital and the willingness to try new things, we are optimistic that this period will leave a strong legacy for the set of energy technologies it has enabled.